Player-Centric Payment Design: Why UX Matters More Than Ever

Explore how player-centric payment design enhances user experience in iGaming, focusing on compliance, mobile optimization, and trust-building features.

A smooth payment experience is now a must for iGaming platforms. Players expect fast, intuitive, and secure payment systems, just like they experience in e-commerce. If a payment process feels clunky or frustrating, players are likely to abandon it - and they might not come back.

Here’s what matters most:

-

Player-first design: Payment systems should feel natural and adapt to player preferences, like remembering favourite payment methods or offering tailored options for high-rollers vs casual players.

-

Compliance withMalta Gaming Authority(MGA): Systems must meet strict security and transparency standards, including clear fees, processing times, and responsible gaming tools.

-

Mobile optimisation: With mobile gaming on the rise, payment flows must work seamlessly on smartphones, offering touch-friendly designs and quick navigation.

-

Trust-building features: Displaying security badges, real-time transaction updates, and transparent currency conversions reassures players.

Malta’s Regulatory and Market Requirements for Payment UX

the thriving iGaming industry demands strict adherence to regulations and a top-notch user experience. Meeting these requirements is essential for crafting payment systems that are both compliant and user-friendly.

Malta Gaming Authority (MGA) Payment Standards

The Malta Gaming Authority (MGA) sets clear expectations for payment systems: they must be secure, transparent, and fair. This includes providing clear information on fees, processing times, and limits. Security is a top priority, requiring multi-layered identity verification processes to protect users.

Additionally, the MGA mandates robust transaction monitoring and reporting systems. Payment interfaces should allow players to review their transaction histories and receive real-time updates on payment statuses. Responsible gaming tools are also a must - features like spending controls, deposit limits, and cooling-off options should be seamlessly integrated to help players manage their activity responsibly.

These foundational standards ensure compliance, but adapting to local market preferences is equally important.

Adapting Payment Systems for the Market

As an EU member state, EU jurisdictions align with European standards, and players expect payment systems to reflect this. For instance, local users are accustomed to European formats for currency (€1,234.56), dates (DD/MM/YYYY), and numbers. Ensuring these formats are implemented correctly is key to maintaining usability.

Language accessibility is another important factor. Payment interfaces should be available in both English and Maltese, ensuring they are easy to navigate for all users.

Mobile gaming is particularly popular in regulated jurisdictions, so payment systems must be optimised for mobile use. This means touch-friendly interfaces, simplified input methods, and clear transaction updates to meet the expectations of players who prefer gaming on the go.

When it comes to payment options, local preferences align with European trends. Support for SEPA transfers, widely used European e-wallets, and secure card processing in line with industry standards is essential. To build trust, payment platforms should include visible regulatory information, up-to-date security certifications, and transparent fee details.

Lastly, Malta’s focus on responsible gaming adds another layer of consideration. Payment interfaces should make tools like deposit limits and spending trackers easy to access, while respecting players’ privacy and autonomy.

Key UX Principles for iGaming Payment Systems

Creating smooth payment processes in iGaming isn’t just about functionality. It’s about recognising that every step counts, from a player’s first deposit to their withdrawal confirmation. These core UX principles are what make payment systems not just functional, but enjoyable to use.

Simple Design and Easy Navigation

When it comes to payment flows, simplicity is king. Players want transactions to be quick and straightforward, with no unnecessary detours. The best systems follow a clear sequence: select amount, choose a method, confirm, and complete.

Keep interfaces clean and uncluttered. Use familiar icons and arrange information logically to reduce confusion. Break down forms into smaller, manageable steps instead of overwhelming players with long ones. A clear visual hierarchy ensures players know exactly what to do next without second-guessing.

If something goes wrong - like a declined card - display messages that are direct and helpful, such as: “Your card was declined. Please check your details or try another payment method.”

Navigation should feel natural and predictable. Players expect to find payment options in obvious places, like buttons labelled “Deposit” or “Cashier.” Tools like breadcrumbs and progress indicators let users see where they are in the process and how many steps remain. By simplifying navigation and addressing errors effectively, you create a payment system that feels both secure and user-friendly.

Security Features and Trust Indicators

Trust is the bedrock of any payment system. Players need to feel reassured that their financial details are safe and that transactions are handled securely.

Prominently display SSL certificates, encryption badges, and compliance certifications to instil confidence. Clearly explain how data is handled and processed. Real-time transaction updates are another way to build trust - when players see their transaction status updating live, they know the system is working as it should. Providing clear timelines for processing transactions also reduces any anxiety about delays.

Keep trust indicators subtle but accessible. For instance, place compliance certifications and security badges in a footer section, ensuring they’re visible without overcrowding the interface. The goal is to make security information available to those who need it, without overwhelming others.

Once trust is established, the next step is ensuring the system adapts to the many ways players access it.

Customisation and Device Accessibility

A secure and intuitive design is only part of the equation. Payment systems also need to work seamlessly across the wide range of devices players use. Whether on desktops, tablets, or smartphones, the experience should feel consistent and easy to navigate.

With many players relying on smartphones, mobile-first design is now essential. This means designing for touchscreens, using large, easy-to-tap buttons, and streamlining input fields. Payment forms should trigger the right keyboard layout for each field, making the process smoother for mobile users.

Allow players to save payment preferences for faster future transactions, but always give them control over what information is stored. Convenience should never come at the expense of privacy.

Accessibility is another crucial factor. Payment systems should support players with different needs by including features like proper contrast ratios, keyboard navigation, and screen reader compatibility. Alt text for images and clearly labelled forms ensure inclusivity for all users.

Device-specific enhancements can also elevate the experience. Mobile users might appreciate biometric authentication options, while desktop users could benefit from detailed transaction histories and advanced filtering tools. The key is to adapt to the context of how and where players are using the system.

Consistency across devices is vital. While the interface may adjust to fit different screen sizes, the core functions and branding should remain the same. This consistency helps players feel at ease, no matter how they access the platform, building familiarity and trust at every touchpoint.

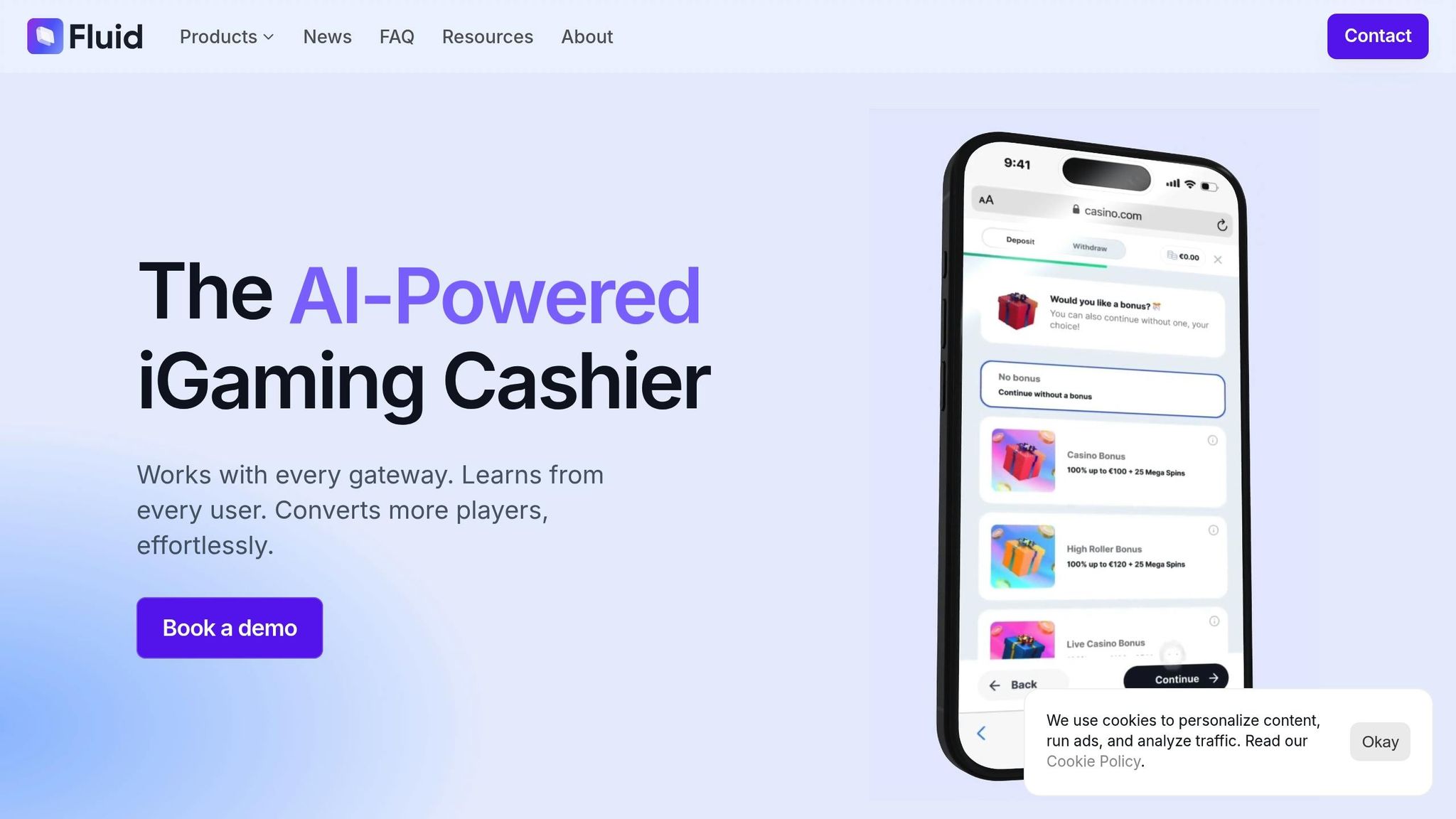

Fluid’s AI-Powered Solutions for Player-Focused Payments

Fluid takes the UX principles we’ve discussed and translates them into practical, player-first payment solutions, all while adhering to the regulatory standards. As an AI-driven digital cashier, Fluid tackles the challenges iGaming operators face in crafting payment experiences that truly centre on the player. By focusing on personalisation, seamless integration, and robust security, Fluid lays the groundwork for boosting player satisfaction.

AI-Powered Personalised Payment Flows

Fluid’s AI doesn’t just process payments - it learns from them. By analysing behaviour, payment history, and preferences, it creates payment experiences tailored to each player. Whether someone needs a detailed view of their transactions or a quick, hassle-free checkout, the system adjusts in real time to meet those needs, cutting down friction and improving conversion rates.

For example, if a player consistently deposits €50.00 using a specific card on weekends, Fluid’s AI remembers this preference. The next time that player logs in, the system prioritises their preferred payment method and suggests similar amounts, making the process faster and more intuitive.

This level of personalisation isn’t just convenient - it directly impacts the bottom line. By reducing unnecessary steps and anticipating user needs, players are more likely to complete transactions, resulting in higher satisfaction and better retention.

Effortless Integration and Real-Time Analytics

Fluid goes beyond personalisation by simplifying technical integration and offering live analytics that help operators fine-tune their systems. Upgrading payment UX can often be a technical headache, but Fluid eliminates this hurdle with smooth integration into existing platforms. Operators can adopt the system without overhauling their current setup or disrupting operations.

Unlike generic solutions that rely on basic iframes, Fluid ensures the payment interface blends seamlessly with the operator’s branding. This keeps the player experience consistent, avoiding any jarring transitions to third-party systems.

On top of that, real-time analytics provide actionable insights into user behaviour, highlighting areas where friction occurs. The data is displayed in familiar, local formats - like €1,234.56 or DD/MM/YYYY - so operators can quickly identify and address performance issues.

Advanced Fraud Detection and Multi-Currency Options

Security is a cornerstone of payment processing, and Fluid’s AI-powered fraud detection system ensures that transactions are both safe and smooth. Using machine learning, the system monitors transactions in real time, adapting continuously to new fraud tactics.

“AI’s role in this process is crucial. It enables a proactive approach to fraud detection, allowing operators to respond swiftly and effectively to potential threats, safeguarding the platform’s integrity and trustworthiness and enhancing the overall user experience by ensuring a secure and fair gaming environment.” - Hlib Kuznietsov, Data Scientist Tech

Fluid’s fraud detection system combines real-time monitoring with multi-layer authentication, offering a strong defence against emerging threats. Additionally, the platform supports multiple currencies, including Dynamic Currency Conversion and cryptocurrency, automatically formatting amounts to local standards. This not only simplifies transactions but also builds trust by providing transparency.

For players, the ability to pay in their preferred currency - while operators maintain clear euro-based records for regulatory purposes - creates a seamless experience. Transparent multi-currency transactions, free from hidden fees or unclear exchange rates, align perfectly with Malta Gaming Authority requirements. By ensuring secure and straightforward transactions, Fluid helps operators build the trust that’s essential for keeping players engaged and satisfied.

Practical Strategies for Better Payment UX in regulated jurisdictions

To improve payment experiences in regulated iGaming markets, it’s essential to blend user-focused design with regulatory compliance. Below are practical strategies that incorporate advanced AI, mobile-first design, and local payment preferences, ensuring a seamless experience for players while adhering to Malta Gaming Authority (MGA) standards.

Using AI for Payment Personalisation

AI is reshaping payment processes by creating customised experiences that adapt to individual user behaviour in real time. By analysing transaction history, preferences, and habits, AI can streamline the checkout journey significantly.

For example, predictive personalisation can pre-fill payment details, cutting down on unnecessary steps. Smart suggestions, like recommending deposit amounts based on past activity, cater to both casual and high-frequency players. Even the timing of payment prompts can be optimised to align with peak activity periods, improving conversion rates and enhancing user satisfaction.

Mobile-First and Accessible Payment Design

In regulated jurisdictions, where mobile usage is prominent, optimising payment systems for mobile devices is non-negotiable. A mobile-first design ensures that payment flows are crafted specifically for smaller screens before being scaled for desktop use.

Touch-friendly designs are key. Interactive elements must be large enough for easy tapping, and layouts should work seamlessly with on-screen keyboards. Features like auto-fill and one-handed operation make actions like “Confirm Payment” effortless. Progressive disclosure, which prioritises the most relevant payment options while keeping others accessible via expandable sections, reduces decision fatigue and speeds up the process.

Accessibility is another critical factor. Payment interfaces should be compatible with screen readers, offer high-contrast modes, and include alternative text for visual elements. Smooth keyboard navigation is essential for users relying on non-touch inputs. Additionally, payment pages should load core content quickly, even on slower networks, while biometric authentication - such as fingerprint or facial recognition - provides a secure and convenient way to confirm payments.

These practices not only create a smoother mobile experience but also ensure inclusivity, setting the stage for integrating local payment methods and robust security measures.

Adding Local Payment Methods and Enhancing Security Compliance

To cater to players in regulated markets, payment options must align with local preferences and banking habits. For instance, traditional bank transfers are often preferred for larger deposits, while e-wallets enjoy widespread use among European players. Integrating SEPA (Single Euro Payments Area) methods is particularly important, as they allow for cost-effective euro transactions without currency conversion fees.

For operators considering cryptocurrency, any integration must strictly comply with the regulatory framework and adhere to guidelines from the Malta Digital Innovation Authority. Building partnerships with local banks can also improve transaction reliability, speed, and fraud detection, while ensuring compliance with local regulations.

Security is a cornerstone of any payment system. Beyond basic measures, achieving PCI DSS compliance and implementing strong customer authentication (as mandated by PSD2) are essential. Continuous transaction monitoring helps meet anti-money laundering requirements, and proper data localisation ensures alignment with GDPR and MGA standards.

Lastly, transparency in fee structures is critical. Clearly displaying charges - like currency conversion or processing fees - not only builds trust but also ensures compliance with consumer protection laws. These measures collectively create a secure, user-friendly payment experience tailored for the unique market.

The Future of Player-Focused Payment Design

In regulated iGaming markets, emerging technologies and rising player expectations are driving significant changes in payment systems.

Artificial intelligence (AI) is already playing a key role by creating personalised payment experiences. By analysing user behaviour, deposit patterns, and risk profiles in real time, AI reduces friction while maintaining the strict security standards set by the Malta Gaming Authority. As AI evolves, these systems will become even more refined, offering smoother and more tailored payment journeys.

Biometric authentication is another game-changer. Fingerprint scanning, facial recognition, and voice authentication are set to simplify verification processes while boosting security. These technologies address the dual challenge of meeting regulatory requirements and ensuring a seamless user experience.

Blockchain technology and digital currencies are also gaining traction. With the Malta Digital Innovation Authority refining its regulatory guidelines, operators can look forward to clearer frameworks for adopting these technologies. This will allow for innovative payment solutions that balance consumer protection with forward-thinking strategies.

Real-time analytics will revolutionise how operators understand and respond to payment behaviour. Advanced tools will provide instant insights into key metrics like conversion rates, abandonment points, and user preferences. This data will empower operators to make quick optimisations, improving both player satisfaction and revenue.

Mobile-first design will continue to dominate, as payment systems are increasingly optimised for smartphones and tablets, while still performing effectively on desktops. This shift reflects the growing preference for mobile gaming among players.

Enhanced compliance measures will also become more integrated into payment systems. Features like advanced transaction monitoring, automated reporting, and anti-money laundering protocols will work seamlessly within the user experience, ensuring that regulatory requirements are met without disrupting gameplay.

Consistency across platforms remains crucial. As players move between devices and channels, synchronising payment preferences, saved methods, and personalisation settings will create a unified experience, no matter how the platform is accessed.

FAQs

How does AI improve personalised payment experiences for iGaming players?

AI significantly improves personalised payment experiences in the iGaming sector by analysing user preferences like preferred devices, locations, and payment methods. This enables platforms to present customised options, making transactions smoother and more user-friendly.

On top of that, AI can anticipate payment preferences based on past behaviours, cutting down on unnecessary steps and boosting satisfaction. It also ensures adherence to local regulations, including GDPR and anti-money laundering laws, which helps build trust and ensures secure transactions for players in regulated jurisdictions.

What are the best strategies for optimising mobile payment systems in regulated iGaming markets?

To enhance mobile payment systems for regulated iGaming markets, it’s essential to prioritise user-friendly and secure payment experiences designed specifically for mobile devices. Focus on creating a responsive interface that works well on smaller screens, with clear buttons and straightforward instructions to ensure players can complete transactions effortlessly.

Integrating localisation features is key. Display prices in euros (€) using the correct format (e.g., €1,234.56) and adopt date formats familiar to licensed users, such as DD/MM/YYYY. Additionally, ensure payment processing is fast and efficient. Offering a mix of popular local payment methods alongside international options can significantly improve convenience and build player trust.

Incorporate AI-driven personalisation to anticipate user preferences and make the payment process even smoother. At the same time, maintain strong security protocols to safeguard sensitive information and enhance player confidence in the system.

How do Malta Gaming Authority (MGA) regulations shape payment system design in the iGaming industry?

The Malta Gaming Authority (MGA) enforces strict regulations to promote transparency, security, and fairness in the iGaming sector. These rules heavily shape how payment systems are designed, requiring operators to implement strict Anti-Money Laundering (AML) protocols, confirm player identities, and closely monitor financial transactions to prevent fraud and ensure regulatory compliance.

To align with these requirements, payment systems need to prioritise secure yet efficient user verification methods without compromising the player experience. Furthermore, operators must ensure that payment processes accommodate the euro (€) as the primary currency and reflect local preferences - such as using the day-month-year (DD/MM/YYYY) date format and appropriate decimal and thousand separators. This approach ensures a system that is both user-friendly and fully compliant for players in regulated markets.